This document analyzes the market shares, market size, and mergers and acquisitions (M&A) activity in the Heating, Ventilation, and Air Conditioning (HVAC) industry in North America. In North America, the market as a whole continues to grow at a robust pace as a result of rising demand due to climate change and sustained urbanization.

In this report, we provide an overview of the key HVAC players active in North America, including Japanese player Daikin and U.S. peers Trane Technologies, Carrier Corporation, Johnson Controls and Lennox International.

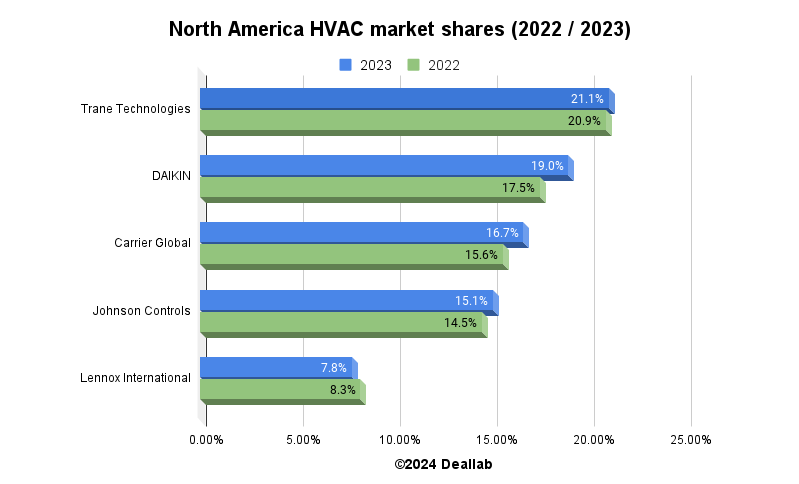

North America HVAC Market Shares (2023)

The market shares can be estimated using the HVAC segment revenue of each HVAC company in North America in 2023 relative to the overall market size estimated in the following section. On that basis, Trane Technologies appears to be the market leader in North America, followed by Daikin, then Carrier.

| Ranking | Company | Market Share |

|---|---|---|

| No. 1 | Trane Technologies | 21.1% |

| No. 2 | DAIKIN | 19.0% |

| No. 3 | Carrier Global | 16.7% |

| No. 4 | Johnson Controls | 15.1% |

| No. 5 | Lennox International | 7.8% |

Source: DealLabs’ estimates of each company’s North American HVAC revenue in January-December 2023 based on annual reports and other data.

Market Share (2021) in North America

.png)

Source: DealLabs’ estimates of each company’s North American HVAC revenue in January-December 2021 based on annual reports and other data.

Comparing the rate of growth in market shares for the leading five players in 2022 and 2023, the market shares of Trane Technologies, Daikin, Carrier, and Johnson Controls have increased, while the market share of Lennox, which holds the fifth largest share, has declined.

The North American air conditioning market as a whole benefitted from factors such as producers passing on higher prices caused by inflation and rising demand in the commercial market, but demand stagnated in the residential market owing partly to persistently high mortgage rates. According to data from the U.S. Department of Commerce, new housing starts are down 12.7% from 2022, affecting the entire North American HVAC industry.

Trane Technologies has maintained its leading market share, as in the previous year. As mentioned above, although revenues from in residential equipment tended to be weak owing to stagnation in the new housing and transportation markets, overall revenues increased as a result of price increases based on inflation and strong demand in the commercial market.

In addition, revenues from the likes of MTA, which Trane Technologies acquired in May 2023, have helped it maintain its leading position and increase market share.

Daikin, in second place, increased its market share from 17.5% in 2022 to 19.0%, and has continued to grow at a much faster pace than other companies in the North American market, as in the previous year. This is likely mainly because, in addition to being selective and focused in its business, such as expanding sales to the manufacturing industry, where the market remains robust, and data centers, where demand is strong, Daikin has made good progress on its strategy of actively using M&A to strengthen supply and sales capabilities, and the company has strengthened the foundations to enable it to actively respond even in difficult market conditions.

According to this database, DealLab estimates the North American HVAC industry was worth $49.6 billion in 2022 and $52.7 billion in 2023. With the market growing by approximately 6.3%, Daikin’s sales have grown at a rapid pace every year, and it is closing the gap with the leading player, Trane Technologies.

The North American market is dominated by duct-type air conditioning systems. This has historically been a barrier to entry for Japanese HVAC players who specialize in ductless air conditioning systems.

In order to expand its range of locally suitable HVAC equipment, Daikin acquired McQuay (OYL Industries), which was strong in large air conditioning systems, in 2008 and Goodman, which is strong in residential air conditioning equipment, in 2012.

In addition, the company is promoting the introduction of products that combine Daikin’s core strengths in energy saving, inverter and refrigerant technologies with duct-type air conditioning systems that are dominant in North America. It appears this is one factor contributing to the steady expansion of the company’s market share.

Since 2020, Daikin has also acquired Abco, Thermal Supply, AirReps, Williams Distributing, Alliance Air Products, CM3 Building Solutions, and other companies. The company is also focusing on strengthening supply capabilities, expanding sales channels, and expansion in the maintenance domain.

Despite the instability in demand in the industry, Daikin is building solid foundations by engaging in local production through the promotion of its M&A strategy, and thereby strengthening its product development, supply capability, and sales network, and this is apparent from the trend in the company’s market share.

Evolution of Daikin’s M&A and Market Capitalization

As described below, along with the expansion of its U.S. operations, Daikin’s market capitalization has also outperformed the Nikkei 225.

-1024x576.png)

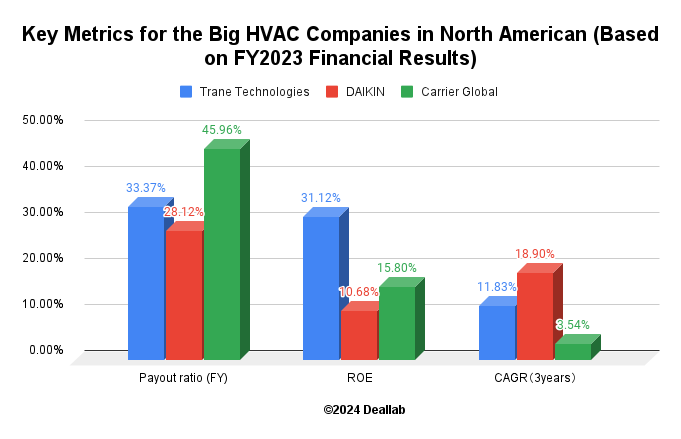

Snapshot of key metrics

The table below summarizes dividend payout ratio, ROE and the revenue growth rates (over the past three years) of Trane Technologies, Daikin and Carrier. Daikin has outperformed competitors in terms of sales growth, Carrier in terms of dividend payout, and Trane in terms of ROE.

*Dividend payout ratio is calculated based on TTM as of June 1, 2024.

**ROE is calculated based on net income for the previous fiscal year and the average amount of shareholders’ equity at the beginning and end of the fiscal year.

***Sales growth rate is calculated as the compound annual growth rate (CAGR) over the past three years.

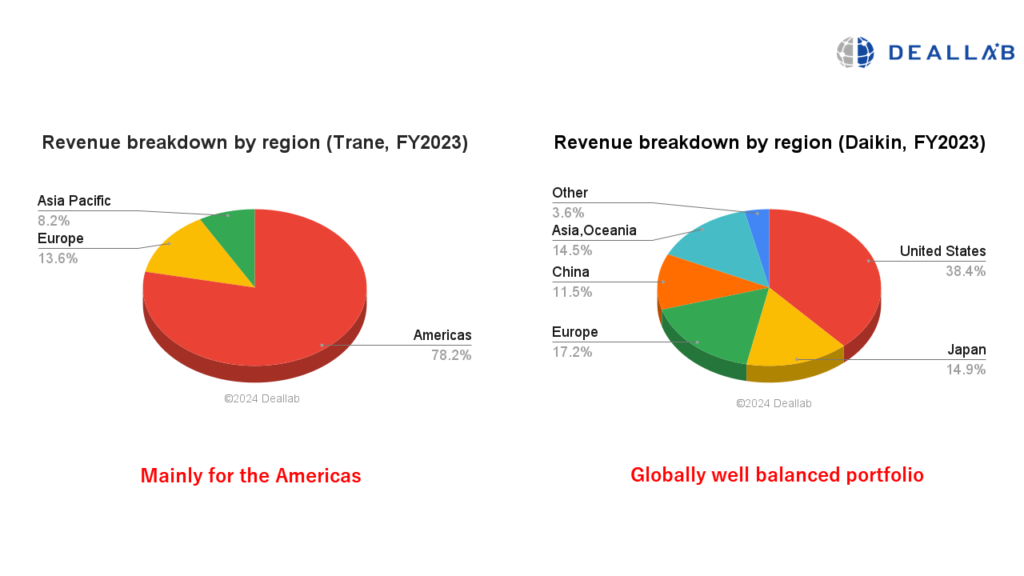

Revenue breakdown by region

Looking at revenue by region, the largest player, Trane Technologies, focuses on the North American and Central/South American markets, while Daikin has a global geographical presence with a strong footprint in China, Japan, and Europe.

The revenue composition of Trane Technologies indicates that even HVAC giants face challenges to expand globally due to differences in consumer preferences and product technologies in each region. However, Daikin has overcome such difficulties and moved ahead of competitors in successfully developing globally as an HVAC player.

Approximately 30 years ago, around 15% of Daikin’s sales were generated overseas, a significant difference from the ratio of overseas sales in 2023. In recent years, Daikin has expanded its production sites and strengthened sales offices in Southeast Asia, the Middle East, Africa, India, and elsewhere.

- 2022: Established an air conditioner production plant in Indonesia

- 2022: Established an assembly plant in Saudi Arabia, its second country in the Middle East

- 2023: Began an air conditioner subscription service in Africa

- 2023: Established an air conditioning sales company in Cambodia

- 2023: Established a new air conditioner production site in India

In addition to North America, there has been a strong focus on global development among major players. In October 2022, Trane Technologies announced the acquisition of AL-KO Air Technology, a major German air conditioning manufacturer, followed by the acquisition of MTA in Italy in May 2023.

In April 2023, Carrier, which holds the third largest market share in North America, announced the acquisition of Viessmann Climate Solutions, a major German air conditioning manufacturer, and significant restructuring is expected to continue on a global basis.

Size of the HVAC Industry in North America in the Global Market

Based on third-party market research data laid out below, DealLab estimates the North American HVAC industry was worth $52.7 billion in 2023.

| Year | market size | Growth Rate |

|---|---|---|

| 2023 | $52.7 billion | 6.25% |

| 2032 | $69.9 billion | 3.19% |

*The Compound Annual Growth Rate (CAGR) is projected for the period between 2023 and 2032.

**The growth rate from 2022 to 2023 is calculated based on the actual data for 2022 in our database.

According to research company Fortune Business Insights, the North American HVAC market was expected to be worth $46.74 billion in 2023. The market was worth $65.76 billion in 2023, according to research company Next Move Strategy Consulting.

According to research company Market Research Future, the size of the market is expected to grow from $45.6 billion in 2023 to $69.9 billion in 2032.

The main reasons for the future growth of the HVAC market in North America are thought to be advancing technological innovation and growing demand for systems with a low environmental impact. Specifically, future market growth is expected to be mainly driven by a response to factors such as regulations to phase out the use of refrigerants with high global warming potential, such as hydrofluorocarbons (HFC), in North America, and measures to reduce the energy consumption of HVAC systems through the establishment of energy efficiency standards in the United States.

Furthermore, as a global environmental factor, cooling demand is increasing in line with a rise in extreme weather events in North America, such as increasingly high temperatures in the summer. According to a report by the U.S. Environmental Protection Agency (EPA), average temperatures have increased over the past few decades, and this appears likely to contribute to future market expansion.

North American Market from a Global Perspective

According to Grand View Research, the size of the global HVAC industry (air conditioning) market was $233.5 billion in 2023. The North American market, estimated by DealLab based on reports by research companies, accounts for approximately 20-30% of the global market size, indicating that it is a huge market. The North American market is also estimated to be about seven times the size of the Japanese market.

Classification of the HVAC Industry in North America in the Global Market

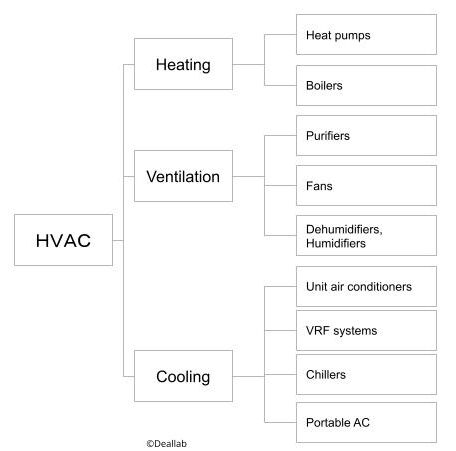

The HVAC market is classified into two segments: the equipment segment, where industry players manufacture and sell HVAC equipment such as heating, ventilation, and cooling equipment, and the solutions segment. In addition to the sale of equipment, in the solutions segment, companies are required to provide efficient energy management of entire facilities and buildings, including maintenance. The segment has been expanding rapidly in recent years.

Heating, ventilation, and cooling equipment is further subdivided into heat pumps, boilers, purifiers, ventilation fans, dehumidifiers and humidifiers, unit air conditioners, VRF systems, chillers, and portable air conditioners.

Selected M&As in North America

- 1979 Acquisition of Carrier by United Technologies

- 2006 Acquisition of Malaysian air conditioning manufacturer OYL by Daikin

- 2008 Acquisition of Trane Technologies by Ingersoll-Rand

- 2011 Acquisition of Carrier’s South American operations by Midea Group

- 2012 Acquisition of Goodman Global by Daikin

- 2014 Acquisition of Air Distribution Technologies (U.S.) by Johnson Controls

- 2016 Management integration of Johnson Controls and Tyco

- 2016 Acquisition of Flanders (U.S.) by Daikin

- 2018 Acquisition of Triatek, a manufacturer of airflow solutions, by Johnson Controls

- 2018 Establishment of a joint venture by Mitsubishi Electric and Ingersoll Rand to sell ductless air conditioners

- 2020 Spin-off of Trane Technologies by Ingersoll-Rand

- 2020 Acquisition of air conditioning dealers Abco, Robinson, and Stevens by Daikin

- 2020 Spin-off of Carrier by United Technologies

- 2021 Acquisition of major air conditioning distributor Temperature Equipment (TEC) by Carrier and major U.S. air conditioning distributor Watsco

- 2021 Acquisition of the Fisher Group, which operates HVAC sales and installation businesses in the U.K., by Johnson Controls

- 2021 Acquisition of air conditioning wholesaler Thermal Supply and commercial air conditioning distributor AirReps by Daikin

- 2022 Carrier made Toshiba Carrier its subsidiary (acquisition of Toshiba Carrier by Carrier subsidiary Global Comfort Solutions LLC)

- 2022 Acquisition of FogHorn AI software by Johnson Controls

- 2022 Acquisition of major U.S. telecoms equipment company Venstar by Daikin

- 2022 Acquisition of major German air conditioning company AL-KO by Trane Technologies

- 2023 Acquisition of major German air conditioning company Viessmann Climate Solutions by Carrier

- 2023 Acquisition of MTA (Italy) by Trane Technologies

- 2023 Acquisition of Alliance Air Products and CM3 Building Solutions (U.S.) by Daikin

- 2023 Acquisition of AES, a U.S. commercial HVAC service provider, by Lennox

- 2023 Acquisition of Nuvolo, a U.S. facilities management solution provider, by Trane Technologies 2023 Sale of commercial refrigeration unit to joint venture partner Haier (China) by Carrier

In terms of trends in M&A in recent years, there have been increases not only in direct acquisitions of air conditioning equipment manufacturers, but also in deals that are expected to expand sales channels and add value to existing air conditioning functions.

The 2022 acquisition of Venstar by Daikin enabled Daikin to offer Venstar’s remote services for air conditioning equipment. Additionally, the 2023 acquisition of Nuvolo by Trane Technologies also provides operational management solutions for buildings and facilities, which is likely to contribute to the development of new sales channels and improvements to energy efficiency.

Furthermore, the restructuring of the HVAC industry may feature participation not only from players in the HVAC industry, but also new players. One possibility is Tesla (U.S.). Heat pump-type systems are increasingly being used for air conditioning in electric and hybrid vehicles to increase energy efficiency. Tesla CEO Elon Musk has mentioned entering the home HVAC industry in a speech to investors, and it is possible that players from other industries will be involved in future restructuring.

Key HVAC players snapshot

Daikin

Daikin is Japan’s leading HVAC manufacturer, founded in 1924. It is one of the world’s top manufacturers of industrial heating and air conditioning equipment. It has expanded its business globally by acquiring Goodman Global, which is strong in duct systems, and OYL, a major air conditioner manufacturer in Malaysia. The company is also engaged in the fluorinated compound and other chemical products business.

Carrier Corporation

Carrier Corporation is a leading U.S.-based HVAC manufacturer. In 2020, Carrier air conditioning operations were spun off from United Technologies, together with elevator (Otis) and aircraft components businesses. The company also has strengths in transportation refrigeration equipment and fire alarms.

Johnson Controls (York International Corporation)

York is a U.S.-based HVAC manufacturer and a subsidiary of Johnson Controls.

Johnson Controls is a U.S.-based company founded in 1885 that provides commercial HVAC control systems, security systems, fire detection systems, and building management services. The company invented the electric thermostat. In 2015, Johnson Controls formed a joint venture with Hitachi Appliances in the HVAC field. In 2016, it merged with Tyco International, which is strong in the fire alarm field. The company operates in 150 countries around the world, offering energy efficiency solutions and various automation businesses. It was strong in the field of automotive batteries but sold the business in 2018.

Trane Technologies

Trane Technologies is a U.S.-based HVAC manufacturer. The company was a subsidiary of Ingersoll-Rand, a U.S.-based manufacturer of transportation temperature control equipment, golf carts, and air compressors, and was spun off as Trane Technologies in 2020.

About Ingersoll-Rand

Ingersoll-Rand, a U.S.-based industrial equipment manufacturer founded in 1871, merged with Gardner Denver, a manufacturer of vacuum pumps, compressors, and other industrial machinery, in 2020. Prior to the merger, the HVAC business was spun off as Trane Technologies.

Top-class companies like Allegion in the security industry and Hussmann in the refrigerated showcase industry (sold to Panasonic in 2015) are spun off from Ingersoll-Rand. It is also strong in compressors and air tools and transport refrigeration equipment. Its golf cart business was sold to Platinum Equity in 2021.

Lennox International

Lennox is a U.S.-based HVAC manufacturer founded in 1895. The company’s strengths lie in the residential and commercial air conditioning as well as commercial refrigeration businesses. In the refrigeration business, Lennox supplies unit coolers, fluid coolers, air-cooled condensers, air handlers and refrigeration rack systems to supermarkets, convenience stores, restaurants, warehouses, and distribution centers.